Navigating Florida’s car accident laws can be complex, especially when it comes to the state’s no-fault insurance system. If you’ve been involved in an accident, understanding how no-fault insurance affects your claim is crucial. Unlike in traditional at-fault states, Florida’s system requires drivers to carry Personal Injury Protection (PIP) insurance, which covers medical expenses and lost wages, regardless of who caused the accident.

At Jimenez Law Firm, we help accident victims understand their legal options and maximize their compensation under Florida’s no-fault system. In this guide, we’ll break down how the system works, what it covers, and when you can step outside the no-fault system to pursue further damages.

What Is Florida’s No-Fault Insurance System?

Florida’s no-fault system requires drivers to turn to their own insurance for coverage after an accident, rather than filing a claim against the at-fault driver. This is designed to speed up the claims process and reduce lawsuits. However, it also limits your ability to seek damages beyond what your PIP policy covers.

History and Purpose of No-Fault Insurance

Florida adopted the no-fault system to reduce the burden on courts by limiting lawsuits for minor accidents. The goal is to ensure faster payouts for medical expenses and lost wages while reducing litigation costs. However, critics argue that the system often favors insurance companies and leaves victims with insufficient compensation. You can explore more about Florida accident claims on our Car Accident Attorneys page.

Key Aspects of Florida’s No-Fault Law:

- Personal Injury Protection (PIP) Coverage: Mandatory for all drivers.

- Covers medical bills and lost wages—regardless of fault.

- Does not cover vehicle damage—this falls under separate insurance.

- Limited ability to sue the at-fault driver unless serious injuries occur.

Minimum Insurance Requirements in Florida

Florida law mandates that all drivers carry:

- $10,000 in Personal Injury Protection (PIP)

- $10,000 in Property Damage Liability (PDL)

While this coverage helps pay for injuries and damages, it often falls short of covering severe accidents, leading many drivers to opt for additional coverage such as Bodily Injury Liability (BIL) and Uninsured Motorist Coverage (UMC). If you’ve been injured in an Intersection Accident, legal guidance can help navigate your claim. For a comprehensive legal framework, consult Florida’s Motor Vehicle No-Fault Law as outlined in the state statutes.

What Does PIP Insurance Cover?

PIP insurance is designed to cover immediate medical costs and income loss after an accident, regardless of who is at fault. Here’s what it typically includes:

1. Medical Expenses

- Covers 80% of necessary medical costs, including hospital visits, surgeries, and rehabilitation.

- Includes chiropractic and physical therapy sessions.

- Must seek treatment within 14 days of the accident to qualify for coverage.

If you’ve suffered serious injuries, such as Spinal Cord Injuries, you may need legal assistance to pursue compensation beyond PIP limits.

2. Lost Wages

- Reimburses 60% of lost income if you cannot work due to accident-related injuries.

- May cover replacement services, such as childcare or housekeeping, if your injuries prevent you from performing daily tasks.

3. Death Benefits

- Provides $5,000 in funeral and burial costs to the policyholder’s family in case of a fatal accident.

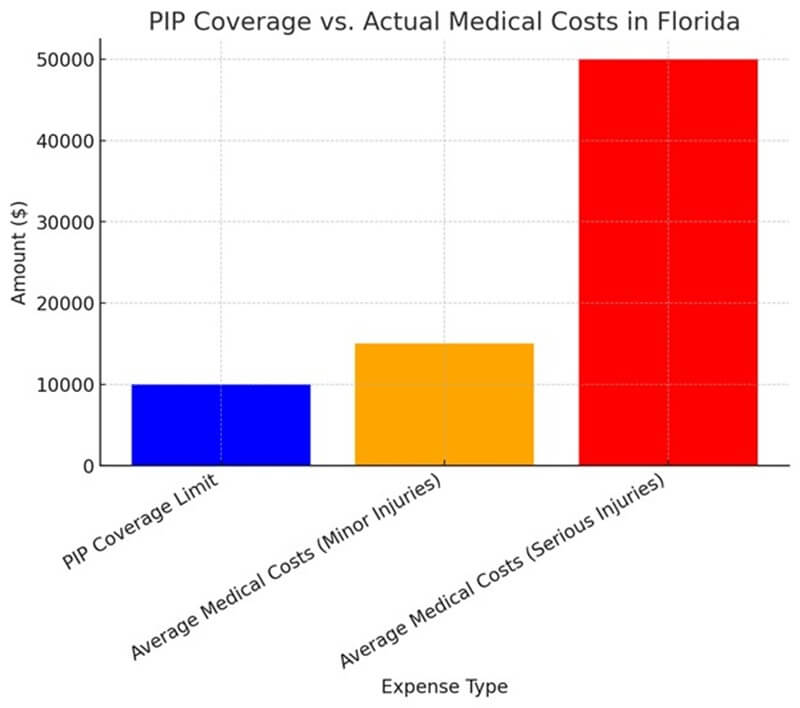

PIP Coverage vs. Actual Medical Costs in Florida

One of the biggest challenges of Florida’s no-fault insurance system is the insufficiency of PIP coverage for many accident victims. While PIP is designed to cover basic medical expenses and lost wages, the reality is that medical costs can quickly exceed the $10,000 limit, leaving victims struggling to cover their bills.

The following chart compares the PIP coverage limit with the average medical expenses for minor and serious injuries in Florida. This visual demonstrates why many drivers seek additional insurance coverage or legal assistance when involved in a car accident.

As the chart shows, medical costs for even minor injuries often exceed the standard PIP coverage limit, and for serious injuries, the expenses can be five times higher than what PIP provides. This financial gap highlights the limitations of Florida’s no-fault system, which we will explore in the next section.

Limitations of Florida’s No-Fault System

While PIP offers essential benefits, it comes with significant limitations:

- Coverage Gaps: The $10,000 limit is often insufficient for serious injuries.

- Limited Compensation: PIP does not cover pain and suffering.

- Higher Insurance Premiums: Florida has some of the highest auto insurance rates in the country due to fraud and the cost of PIP claims.

To see how these limitations impact Hit-and-Run Accidents, check out our in-depth resource.

Additionally, a recent study by the Insurance Information Institute highlights how PIP fraud contributes to increased insurance premiums in Florida.

When Can You Step Outside the No-Fault System?

While Florida’s no-fault system limits lawsuits, you can file a personal injury claim against the at-fault driver if your injuries meet the serious injury threshold. This includes:

- Significant and permanent loss of an important bodily function

- Permanent injury

- Scarring or disfigurement

- Death

If your injuries qualify, you may be able to seek compensation for:

- Medical bills exceeding PIP limits

- Pain and suffering

- Full lost wages and loss of future earnings

Common Issues with No-Fault Insurance Claims

Despite its intended efficiency, Florida’s no-fault insurance system can be challenging. Here are some common issues policyholders face:

1. Denied or Delayed Claims

- Insurance companies may deny claims based on incomplete paperwork, missed deadlines, or disputes over medical necessity.

- Claims may be delayed due to lengthy investigations.

2. Insufficient Coverage

- Florida’s $10,000 PIP limit is often inadequate for serious injuries.

- Many drivers purchase additional coverage, such as Bodily Injury Liability (BIL) and Uninsured Motorist Coverage (UMC), to protect themselves.

3. Disputes Over Medical Expenses

- Insurance companies may challenge whether treatments were medically necessary, leading to partial reimbursements.

- Seeking treatment from PIP-approved providers can help avoid these issues.

How Jimenez Law Firm Can Help

At Jimenez Law Firm, we have extensive experience handling car accident claims in Florida’s no-fault system. Our legal team can help you: ✔ File a PIP claim and handle insurance disputes. ✔ Determine if you meet the serious injury threshold for additional compensation. ✔ Negotiate with insurance companies for fair settlements. ✔ Pursue legal action if your claim is wrongfully denied.

For clients involved in DUI Accidents, legal support is critical in obtaining the compensation you deserve.

Call us at (904) 559-5600

Visit: Jimenez Law Firm

Location: 1443 San Marco Blvd. Suite 201, Jacksonville, FL 32207

Conclusion

Florida’s no-fault insurance system can be confusing, but understanding how it affects your accident claim is essential. If your damages exceed PIP limits, you may have legal options to pursue further compensation.

At Jimenez Law Firm, we fight for accident victims’ rights, ensuring they receive the maximum compensation they deserve. If you need legal assistance with a no-fault insurance claim, contact us today for a free consultation.

Your road to justice starts here.