Car accidents are stressful, even if the damage is minor. Amid the physical shock and emotional toll, dealing with insurance companies can feel like a daunting maze. One wrong step can reduce your settlement or even jeopardize your claim entirely.

At Jimenez Law Firm, we’ve seen how proper post-accident strategies make all the difference—especially when it comes to handling insurance companies. This blog will walk you through key tips to avoid common mistakes and ensure you get the compensation you deserve. If you’re still processing a serious collision like a hit and run, you might find our guide on how to handle a hit-and-run accident in Florida helpful.

Step 1: Prioritize Your Safety and Health First

Before thinking about insurance, your safety and the safety of others should be the top priority. Move to a safe location if possible, check for injuries, and call emergency services. Even if you feel fine, it’s essential to seek medical attention. Some injuries, like whiplash or concussions, can take time to show symptoms.

Why this matters: Insurance companies can use delays in medical treatment as an excuse to question the severity of your injuries or deny your claim. Prompt documentation ensures a strong foundation for your case. For a deeper dive into how Florida’s laws affect injury compensation, check out Florida’s no-fault insurance system.

Step 2: Document Everything at the Scene

Evidence is your best defense. Immediately after the accident, start collecting information. Use your smartphone to take pictures and videos of:

- Vehicle damage (yours and others involved)

- License plates

- The accident scene, including skid marks, road signs, and weather conditions

- Injuries, if visible

- Insurance cards and driver’s licenses

Also, gather contact details from witnesses. If they’re willing, a recorded statement on your phone can be invaluable.

Pro Tip: Use a note-taking app to write down your recollection of the incident while it’s fresh in your mind. This can come in handy when dealing with complex liability issues like intersection accidents.

Step 3: Notify the Police and Get a Report

Even for minor fender-benders, a police report creates an official record. It includes details such as time, date, location, involved parties, and sometimes even officer-assessed fault.

Why it matters: Insurance adjusters may attempt to twist the narrative. A police report serves as a credible third-party account and can prevent “he said, she said” scenarios.

Step 4: Notify Your Insurance Company Promptly

Most insurance policies require you to report accidents promptly. Delaying this step can hurt your ability to file a claim. When contacting your insurer:

- Stick to the facts

- Avoid admitting fault

- Don’t speculate about what happened

What to share: Time and location of the accident, people involved, police report number (if available), and injuries sustained.

If the accident involved a rideshare vehicle, be sure to review your rights related to ridesharing accidents in Florida.

Step 5: Understand the Role of Insurance Adjusters

Insurance adjusters are trained to investigate claims, but their ultimate goal is to minimize the amount their company pays. They may appear sympathetic, but remember:

- You are not required to provide a recorded statement

- They may attempt to pressure you into quick settlements

- Their job is not to advocate for your best interest

What you should do: Be polite, document all communication, and don’t provide statements until you speak to a lawyer. You can learn more about this in our insurance and third-party claims article.

Step 6: Don’t Accept the First Settlement Offer

It’s common for insurance companies to offer a quick payout in hopes of closing the case fast. But:

- These offers rarely consider long-term medical expenses or future pain and suffering

- They may not cover ongoing therapy, lost income, or diminished earning capacity

What to do instead: Request a full itemized breakdown of how the settlement was calculated and compare it with your records. Negotiate or involve an attorney to ensure fairness. For more information on how settlements are calculated, check our post on types of damages.

Thanks for the heads-up! Since the previous Reuters link no longer works, here’s an alternative credible source and updated context that fits seamlessly into your blog:

According to a Forbes Advisor report on auto insurance trends, insurers are tightening their claim evaluations and raising premiums due to inflation and increasing repair costs—making professional legal help more important than ever.

Step 7: Keep Detailed Records of Everything

Thorough documentation will strengthen your claim. Include:

- Emergency room and follow-up visit records

- Prescription receipts and medical bills

- Car repair estimates and towing invoices

- Lost wages documentation

- Communications with insurance companies (emails, texts, letters)

Organize these in a digital folder with backup copies. These documents help prove the extent of your damages and show consistency in your recovery process.

Step 8: Be Cautious of Social Media Activity

In today’s digital world, insurance investigators often scour claimants’ social media profiles. What you post can come back to haunt you.

Example: Posting a video of you dancing at a party after filing a back injury claim could be used to deny compensation.

Best practice: Avoid discussing the accident or your injuries online. Temporarily switch your profiles to private if necessary. To better understand what not to do, read about common legal mistakes after accidents.

Step 9: Consider Legal Representation

Navigating insurance claims, especially those involving injuries, legal jargon, and technicalities, is not easy for most people. Hiring a personal injury lawyer can help in several ways:

- Prevents you from making damaging statements

- Maximizes your compensation by identifying every recoverable expense

- Speeds up the negotiation process

- Takes the pressure off your shoulders so you can focus on healing

When to contact a lawyer:

- You suffered serious injuries

- The other party is disputing fault

- You’re unsure about how much your claim is worth

At Jimenez Law Firm, our legal experts can evaluate your case and communicate with insurers on your behalf. Explore our full range of car accident legal services for more specific case types.

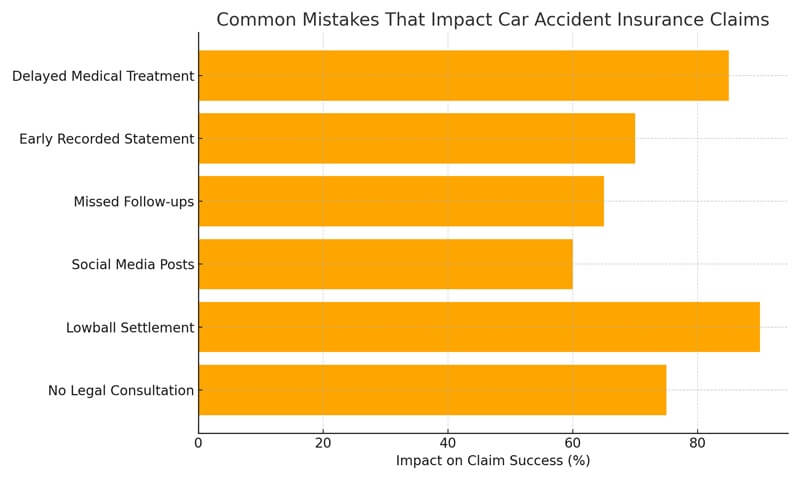

Step 10: Know the Pitfalls to Avoid

Avoid these common post-accident mistakes that can jeopardize your claim:

- Delaying medical treatment: Creates doubt about your injuries

- Providing recorded statements too early: Can be used against you

- Ignoring follow-up appointments: Signals lack of seriousness about recovery

- Posting on social media: May contradict your official claims

- Accepting lowball settlements: Cuts you off from future compensation

- Failing to consult a lawyer when needed: Can cost you significantly

Extra Tips: Navigating Insurance with Confidence

Understand Comparative Fault Laws: Depending on your state, if you’re found partially at fault, your compensation might be reduced. Your attorney can help argue against unfair assessments of fault.

Use a Claims Journal: Keep a daily log of pain levels, mobility limitations, and emotional distress. This can be powerful evidence for non-economic damages.

Avoid Talking to the Other Driver’s Insurer Directly: Always redirect them to your attorney or insurance adjuster.

For more on protecting yourself legally, visit our post about filing lawsuits after an auto accident.

Visual Breakdown: Here’s a look at how common mistakes can impact your insurance claim success rate:

Final Thoughts: Knowledge Is Power

Handling insurance companies after a car accident is all about preparation and awareness. The more informed you are, the harder it becomes for insurance providers to take advantage of you. Prioritize your health, document everything, and don’t rush into decisions.

When in doubt, seek professional legal guidance. With the right support, you can focus on recovery while an expert ensures your rights are protected.

About Jimenez Law Firm

At Jimenez Law Firm, we care about the well-being of our clients and community. That’s why we offer skilled legal representation to those injured in car accidents. We’re more than just legal professionals—we’re here to help you get your life back in order, both physically and emotionally.

Need Legal Support?

Contact Jimenez Law Firm today for a consultation and let our team of experienced attorneys help you navigate the complexities of dealing with insurance companies after an accident.

Here are 6 well-optimized and relevant FAQs to include in your blog post:

FAQs

- What should I say to an insurance adjuster after a car accident?

Stick to the basic facts like date, time, location, and parties involved. Avoid speculating, admitting fault, or discussing your injuries in detail before speaking with an attorney. - Can I refuse to give a recorded statement to the insurance company?

Yes, you have the legal right to decline giving a recorded statement, especially to the other party’s insurer. It’s best to consult with a lawyer first to avoid saying something that could harm your claim. - How soon should I contact my insurance company after an accident?

You should report the accident to your insurance company as soon as possible—ideally within 24 hours—to comply with your policy and avoid delays in the claim process. - What happens if I accept the insurance company’s first settlement offer?

Accepting a settlement means you forfeit the right to seek additional compensation later, even if you discover new injuries or costs. It’s important to have a lawyer review any offer before accepting. - Can social media really affect my insurance claim?

Yes, insurance companies often review claimants’ social media profiles. Posts that contradict your injury claim can be used to deny or reduce your settlement.

6. When should I hire a lawyer after a car accident?

Hire a lawyer immediately if you have serious injuries, the fault is disputed, or the insurer is pressuring you to settle quickly. An attorney will protect your rights and help secure fair compensation.