Introduction: The Harsh Reality of Florida Roads

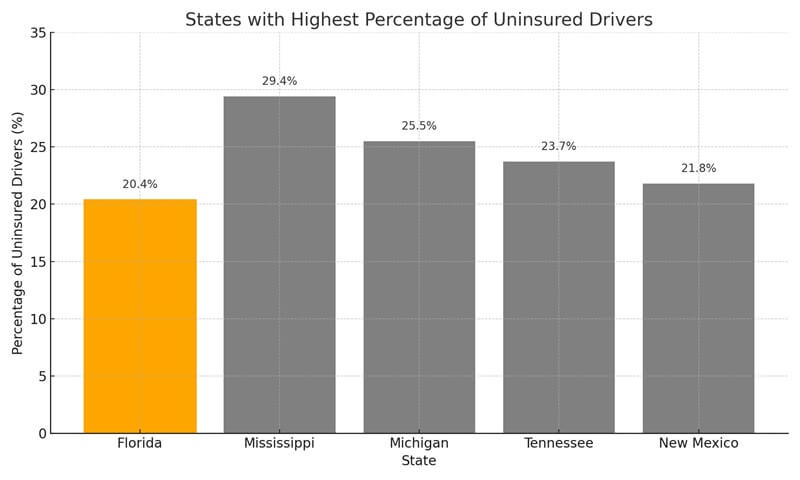

Florida has one of the highest rates of uninsured drivers in the United States. According to the Insurance Research Council, over 20% of drivers in Florida operate a vehicle without proper insurance coverage. This alarming statistic makes it increasingly likely that if you’re involved in a car accident in Florida, the other driver may not have enough insurance — or any at all — to cover your damages.

According to national data, Florida consistently ranks among the top states with the highest percentage of uninsured drivers.

Figure: Florida is among the states with the highest number of uninsured drivers, increasing risk for responsible motorists.

So, what happens if you’re hit by an uninsured or underinsured driver? Can you still get compensated for your medical bills, lost wages, and vehicle damage? At Jimenez Law Firm, we help clients navigate these complex situations and ensure they don’t bear the financial burden of someone else’s negligence. You can also learn more about common legal challenges in these scenarios on our Common Legal Questions page.

Understanding Florida’s No-Fault Insurance System

Florida is a no-fault state, which means that your own insurance company covers your initial medical expenses and lost wages, regardless of who caused the accident. This is done through your Personal Injury Protection (PIP) coverage, which is mandatory in Florida and typically covers:

- Up to 80% of medical expenses

- Up to 60% of lost income

- A portion of essential services like housekeeping or transportation

However, PIP has limits (usually $10,000), and it doesn’t cover non-economic damages like pain and suffering. For a full understanding of this system, check out our article on Florida’s No-Fault Insurance System.

What Is Uninsured/Underinsured Motorist (UM/UIM) Coverage?

This is where Uninsured/Underinsured Motorist (UM/UIM) coverage becomes crucial. While not required in Florida, it is highly recommended. UM/UIM coverage helps pay for damages when the at-fault driver has no insurance or lacks sufficient coverage to fully compensate you.

UM/UIM may cover:

- Medical expenses exceeding PIP limits

- Lost wages beyond PIP

- Pain and suffering

- Future medical care

- Emotional distress

- Permanent disability or disfigurement

UM/UIM can be stacked or non-stacked. Stacked coverage allows you to combine the UM limits of multiple vehicles on your policy, potentially increasing the compensation available. If you’re unsure about your coverage, read our breakdown of Types of Damages you may be entitled to.

Scenarios Where UM/UIM Coverage Is Essential

Let’s say you’re driving through Miami and another driver runs a red light, crashing into your car. You suffer a broken leg and are unable to work for six weeks. The other driver has no insurance. Your PIP coverage may run out quickly due to hospital and rehab bills. If you have UM/UIM, you can recover the remaining medical bills and lost wages, plus additional damages for pain and suffering.

Alternatively, if the other driver only carries Florida’s minimum $10,000 in property damage liability (PDL) and no bodily injury coverage, you could be left with a hefty bill — unless you have UIM coverage.

Another example: If you’re involved in a hit-and-run accident, and the other driver is never identified, UM coverage may be the only way you can recover damages. We explain this further in our post on Hit-and-Run Accidents in Florida.

Filing a UM/UIM Claim: What to Expect

Filing a UM/UIM claim isn’t always straightforward. Insurance companies often scrutinize these claims heavily since they involve paying their own policyholder. Here’s what the process generally looks like:

- Notify your insurer of your intent to file a UM/UIM claim

- Provide documentation such as police reports, medical records, and proof of the other driver’s lack of coverage

- Negotiate the settlement (you may face pushback or low offers)

- Hire an attorney to advocate on your behalf if your claim is delayed, denied, or undervalued

Delays are common with UM/UIM claims, as insurers may challenge the extent of your injuries, argue comparative fault, or downplay long-term consequences. If you’re looking for a deeper explanation of this process, our guide on Insurance and Third-Party Claims can help.

The team at Jimenez Law Firm has extensive experience handling these claims and can help ensure your insurer treats you fairly.

Legal Options Beyond Insurance

If you don’t have UM/UIM coverage, and the at-fault driver is uninsured, you may still have legal options, though they can be more challenging:

- File a personal injury lawsuit against the at-fault driver: This requires proving negligence and demonstrating the financial impact of your injuries.

- Pursue a court judgment: Even if successful, collecting from an uninsured driver is difficult unless they have assets or income that can be garnished.

- Lien or wage garnishment: If the driver has steady income or property, your attorney may pursue post-judgment collection methods.

This is why working with a skilled personal injury attorney is essential. At Jimenez Law Firm, we can assess the viability of a lawsuit and explore all recovery options available to you. Learn more about our Car Accident Attorneys and how we can assist.

Common Pitfalls to Avoid

If you’re dealing with an uninsured or underinsured motorist, avoid making these mistakes:

- Accepting the first offer from your insurance company without legal review

- Failing to gather proper documentation (medical records, witness statements, crash reports)

- Not seeking legal advice early

- Assuming the at-fault driver will pay out-of-pocket

- Ignoring the importance of UM/UIM coverage until it’s too late

You can explore more real-world legal decisions in our article on Florida Slip and Fall Court Decisions.

How a Personal Injury Lawyer Helps You Win Your Case

Navigating post-accident claims is complicated, especially when uninsured drivers are involved. A seasoned personal injury lawyer can:

- Investigate the accident thoroughly and collect vital evidence

- Negotiate with your insurance company for fair compensation

- Represent you in court if a lawsuit is necessary

- Ensure all procedural rules and deadlines are followed to protect your rights

At Jimenez Law Firm, our approach is client-first. We treat every case with the care and determination it deserves. Learn how our Rear-End Accident attorneys can help in specific crash scenarios.

According to a recent Forbes report, uninsured motorist coverage is one of the most overlooked yet essential protections drivers can have.

Why Choose Jimenez Law Firm?

We are passionate about protecting Florida drivers from the financial stress that follows an accident. Our legal team will:

- Review your insurance policies and explore all coverage options

- Handle all communication with insurers

- Fight for full and fair compensation

- Guide you every step of the way

We have successfully represented victims of accidents involving uninsured and underinsured drivers, securing compensation even when hope seemed lost.

What to Do Immediately After an Accident

If you suspect the at-fault driver is uninsured or underinsured, follow these steps:

- Call the police and get an accident report

- Seek immediate medical attention

- Document everything at the scene

- Notify your insurance company but avoid giving a recorded statement until you talk to a lawyer

- Contact Jimenez Law Firm for a free consultation

You can also learn about injuries from related scenarios, like Passenger Injuries, and how to legally protect yourself.

Final Thoughts: Protect Yourself Before It Happens

While you can’t control what other drivers do, you can control how well you’re protected. Review your insurance policy and strongly consider adding UM/UIM coverage if you haven’t already. It could be the safety net you desperately need in the aftermath of an accident.

Understanding your rights and options after a crash with an uninsured driver can make all the difference in your financial and emotional recovery. Educating yourself ahead of time can also prevent serious complications.

If you’ve already been in an accident involving an uninsured or underinsured driver, don’t navigate this alone. Jimenez Law Firm is here to help you explore every possible avenue for compensation and peace of mind.

Need Help? Contact Us Today.

If you or a loved one has been hit by an uninsured or underinsured driver in Florida, contact Jimenez Law Firm today at https://www.jimenez-lawfirm.com/ for a free consultation. We’ll fight to ensure you get the compensation you deserve.

Frequently Asked Questions (FAQs)

- What should I do immediately after an accident with an uninsured driver? Call the police, seek medical attention, document the accident, and contact your insurance provider. Also, consult an attorney before making any statements.

- Can I sue an uninsured driver in Florida? Yes, you can file a personal injury lawsuit against an uninsured driver. However, recovering damages can be difficult unless the driver has assets or income.

- What does UM/UIM insurance cover in Florida? Uninsured/Underinsured Motorist coverage pays for medical bills, lost wages, and pain and suffering if the at-fault driver lacks sufficient insurance.

- Is UM/UIM coverage mandatory in Florida? No, but it’s highly recommended. Without it, your options for recovering damages may be limited.

- Will my insurance premiums increase if I file a UM/UIM claim? Not necessarily. Since you are not at fault, your rates should not increase—but this can vary by insurer and circumstance.

6. How long do I have to file a UM/UIM claim in Florida? The statute of limitations for personal injury claims in Florida is typically four years. However, it’s best to consult an attorney as soon as possible.